“I Need To Sell My House Now!”

We are Homebuyers Specializing in Full Price Offers

If you want to sell your house… we’re ready to give you a fair All-Cash Offer, or a Full Price Offer if you qualify for our programs

Stop the frustration of your unwanted property. Let us buy your property now, regardless of condition or situation.

Avoiding foreclosure? Facing divorce?

Moving? Upside down in your mortgage?

Payments getting hard to make?

It doesn’t matter whether you live in it, you’re renting it out, it’s vacant, or not even habitable. We want your property!

We help owners who have inherited an unwanted property, or own a vacant house, or are tired of being a landlord, or are behind on payments, or need to downsize but can’t sell… even if the house needs repairs that you can’t pay for… and yes, even if the house is fire damaged or has bad rental tenants.

And…(I found this out the hard way myself), did you know that if a house is vacant for more than 30 days, and there is a fire or someone gets hurt on your property, your insurance company will most likely NOT honor your claim?? I was flabbergasted that they could get away with this after all those premiums they’d been happy to deposit over the years.

If you have a property and need to sell it, we’d like to make you a fair offer and close on it when you’re ready.

Listing Your House Can Be A Huge Risk

Selling a house through an agent is not for everyone, but for some it is.

If you would do better getting listed on the MLS, we’ll let you know.

Our general contractor can get do the repairs and upgrades your property needs to be ready for a retail sale… even if you don’t have the money up front, we can work with you. But you may just want a quick cash sale because…

you don’t need to clean up and repair the property

don’t waste time waiting for a retail buyer and hoping they can qualify for a loan

or deal with all the paperwork

All that hassle can add stress, months to the process, and in the end after paying commissions, you may or may not be ahead of the game.

We'll know very quickly if we can help you.

Unlike selling through an agent, you don’t have to wait to see

if the buyer can get financing…

We're ready to buy right now!

We work differently at NQ Capital, Inc.

When you contact us and submit the short property information form (above), we’ll give you a fair offer on your house within 24 hours…

and the best part is…

We can close whenever YOU choose to close – it’s entirely up to you.

It doesn’t matter what condition the house is in, or even if there are tenants in there that

you can’t get rid of… don’t worry about it. We’ll take care of it for you. And if you need

the cash quickly, we can close in as little as 7 days because we buy houses fast

with cash and we don’t have to rely on traditional bank financing.

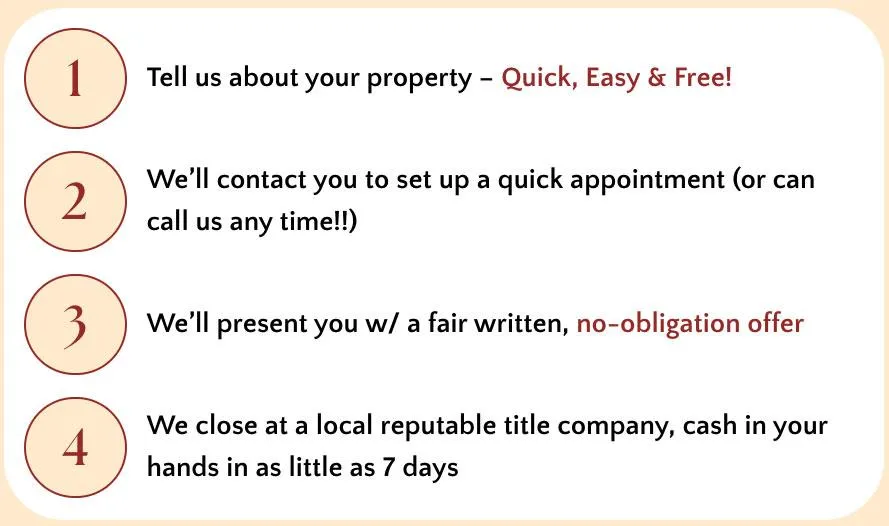

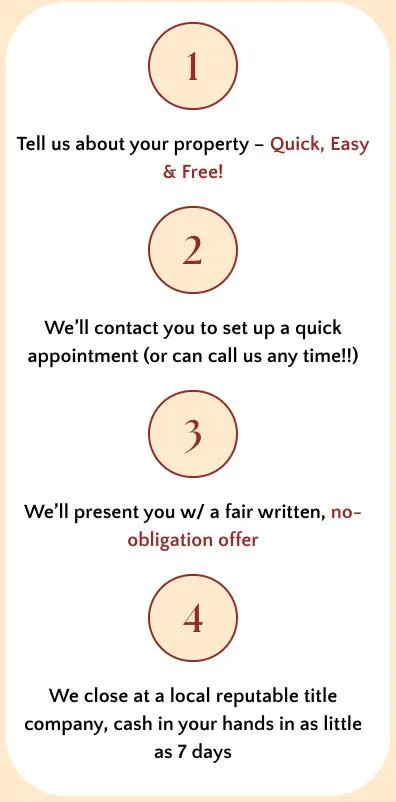

How the Process Works:

Timeframe: Once we get your info, we’re usually able to make you a fair offer within 24 hours. [Please be sure to review our FAQ section below. You need to understand that we operate a bit differently than most companies… we have several options we can offer you]. From there, we can close as quickly as 7 days… or on your schedule (sometimes we can have a check in your hand the very same day!).

Selling Your House Can Be A Quick And Simple Process

NQ Capital, Inc. buys houses in and around Carson City (and across the country!!). We can pay cash for houses we’re able to close quickly… or on your schedule.

Like we’ve mentioned, when you sell for cash, there are no fees. What this means to you is you don’t have to worry about extra costs, having to come out of pocket for repairs and upgrades… we’ll buy your house as-is, and sometimes pay your closing costs as well!

Need help getting your property ready for market? Our general contractor can make quick work of that. We can fix it up so your property sells for more.

No matter what condition your house is in; no matter what situation or timeframe you’re facing…

Our goal is to help make your life easier and get you out from under the property that’s stressing you out…

while still paying a fast, fair, and honest price for your house.

About NQ Capital, Inc.

We are family owned and operated, providing win-win solutions to help homeowners get out of sticky situations… like foreclosure, an inherited property, a troublesome rental or a property that isn’t selling as expected.

My name is Dawn Rickabaugh, and I used to work as an ER nurse. I loved it, but I was ready for a change. I have worked for myself since 2004.

I used to save lives in the ER. Now I help people solve financial and real estate problems. Since moving to Carson City in 2014, we’ve been able to help many families to both sell homes, and buy them both locally and across the country.

We buy both property and paper (real estate and notes).

How We Work With Homeowners

If you have any questions about how we work, what the process of selling a house or having us help you avoid foreclosure, or just want to learn more about us… don’t hesitate to contact us anytime! You will want to review our FAQs below.

Frequently Asked Questions

Q: Will you be listing my house on the MLS or actually buying it?

A: Great question. While we do have a fabulous real estate broker on our team and can do a great job listing your property for a retail sale, many sellers really just want us to buy their home quickly. We are professional home buyers… we buy houses in Carson City, Dayton and surrounding areas.

Once we’re on title we will do one of three things:

Repair the house and resell it to another family in town who can pay cash or get a bank loan

Sell to a good family who has a strong down payment but cannot get a bank loan… for them, we will offer owner financing and ‘become the bank’ so they can escape the rent cycle & finally own something, creating stability for their families

Keep it as a rental for long term cash flow

Q: Does a ‘quick sale’ mean this is some sort of scam? How do I know I’ll be protected?

A: We use title and escrow just like every other respectable real estate transaction. This is the only way to make sure that we’re BOTH protected. Once we come to an agreement, I drop off the signed contract at the escrow company (my favorite escrow officer is Liz Svenningsen @ First Centennial) along with my earnest money deposit. From there, she orders the preliminary title report. Once she can prove that you have clear title (that there are no surprise liens or judgments attached to the property), then she asks us for the rest of the money. Once she has ALL of it in her account, she’ll record the deed from you to us in public record and release your money to you via wire or check, however you want it.

Q: Do you pay fair prices for properties?

A: When we pay ALL CASH, the houses we purchase are below market value (we do this so we can resell it at a profit to another home owner… it’s how we put food on the table). We are looking to get a fair discount on a property. Hopefully you understand that we need to be compensated for the time & money we invest and the risk we take that the market could drop before we get a chance to turn it around.

In our experience, most sellers understand this and aren’t necessarily expecting a large “windfall” but rather appreciate that we can offer cash, close quickly (no appraisals or loan contingencies), and don’t require them to deal with existing tenants, make repairs or pay agent fees (unless, of course, you ask us to list your property instead of buy it).

We can often make a FULL PRICE OFFER if you will work with us on ‘terms’, meaning you are flexible in giving us a little time to get you all of your equity. Your equity is the ‘as is’ value of your property less the balance of any loan you still have against it, (i.e. if your home is worth $400,000 and you still owe the bank $300,000, then your equity is $100,000).

If you see value in what we have to offer, let’s see if we can come to a fair win-win price. When we meet with you, we will explain several ways that we can work together:

Fair cash offer. We will close quickly (or on your timeline).

Owner financing offer. You can get MUCH more for your property if you are willing to let us buy it over time. Yes, you CAN sell all cash and put a big chunk of change in the bank, but you may discover that you’d rather have hassle-free monthly income and make 10 times what the banks will give you on your savings account. You may save on capital gains as well.

We can have our general contractor fix up your home. We can do the repairs so you can list it on the MLS for the highest offer possible. If you don’t have the money up front for repairs, we can work with you.We can list your property. We will list your property on the MLS and get you the best retail offer available in today’s market, if that’s what will serve you best.

We would love to help you get the results that are right for you. Please call now!!

Q: How do you determine the price to offer on my house?

A: Great question, and we’re an open book: Our process is very straightforward. We look at the location of the property, what repairs are needed, the current condition of the property, and values of comparable houses sold in the area recently. We take many pieces of information into consideration… and come up with a fair price that works for us and works for you too. Remember, we can usually offer a higher price if you are willing to “be the bank” and let us pay you over time for your property.

Q: Are there any fees or commissions to work with you?

A: Unless you ask us to list your property, there are NO fees or commissions when you sell your house to us. We’ll make you an offer, and if it’s a fit then we’ll buy your house (and we’ll often pay for the closing costs too!). No hassle. No fees. We make our money after we pay for repairs on the house (if any) and sell it for a profit (we’re taking all of the risk here on whether we can sell it for a profit or not, once we buy the house from you… the responsibility is ours and you walk away without the burden of the property and it’s payments… and often with cash in your hand).

Q: How is it different if I just want to you buy my house instead of list it?

A: Real estate agents list properties and hope that someone will buy them. The agent shows the properties to prospective buyers and then takes a percentage of the sale price when they find a buyer. Oftentimes, the agent’s commission is 5-6% of the sale price of your house (so if it’s a $100,000 house, you’ll pay between $5,000 – $6,000 in commissions to an agent). Agents provide a great service for people that: 1) have a turn-key property that needs no repairs or updating, 2) can wait as long as it takes to sell, and 3) don’t mind the sales process, open houses, paperwork, and paying commissions. If we buy your house instead of list it, we can make a decision to buy within hours.

Q: What if I still have a loan on my property and not much equity?

A: Even if you have little or no equity, but just want out from under your payments without a short sale or foreclosure on your record, we may be able to offer you a solution. If you have good underlying financing in place, and aren’t too far behind on your payments, there’s a good chance we can work together. Sometimes people don’t want to hire an agent because they don’t have enough equity to cover the commissions. That’s a great time to reach out to us to see what we can do together.

Q: Is there any obligation when I submit my info?

A: There is absolutely zero obligation for you. Once you tell us a bit about your property, we’ll take a look at things, maybe set up a call with you to find out a bit more, and make you an all-cash offer that’s fair for you and fair for us. From there, it’s 100% your decision on whether or not you’d like to sell or list your house with us… and we won’t hassle you, won’t harass you… it’s 100% your decision and we’ll let you decide what’s right for you.

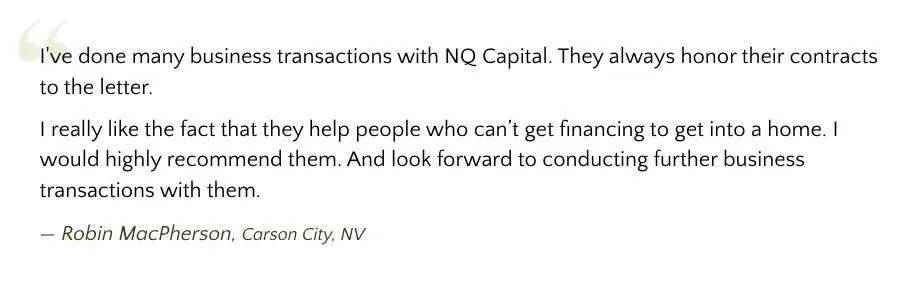

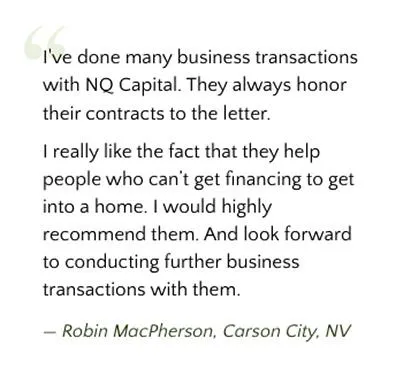

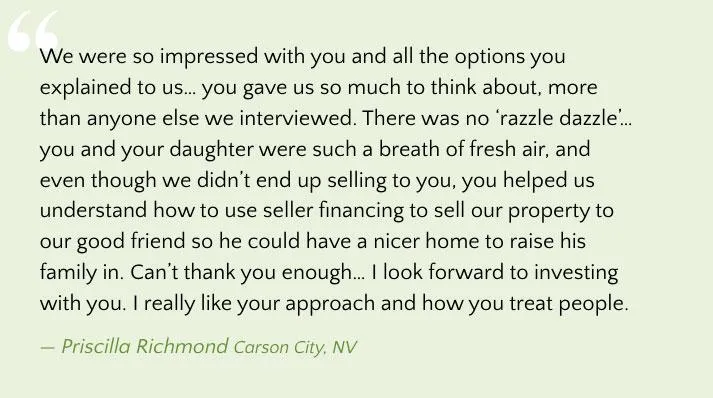

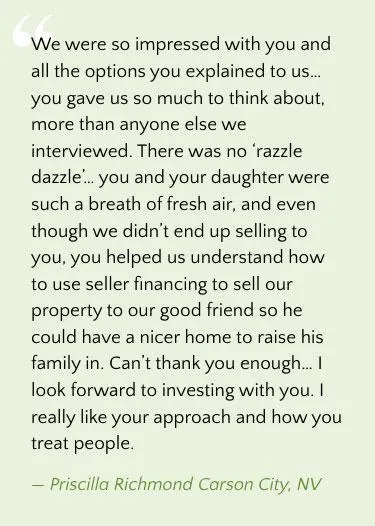

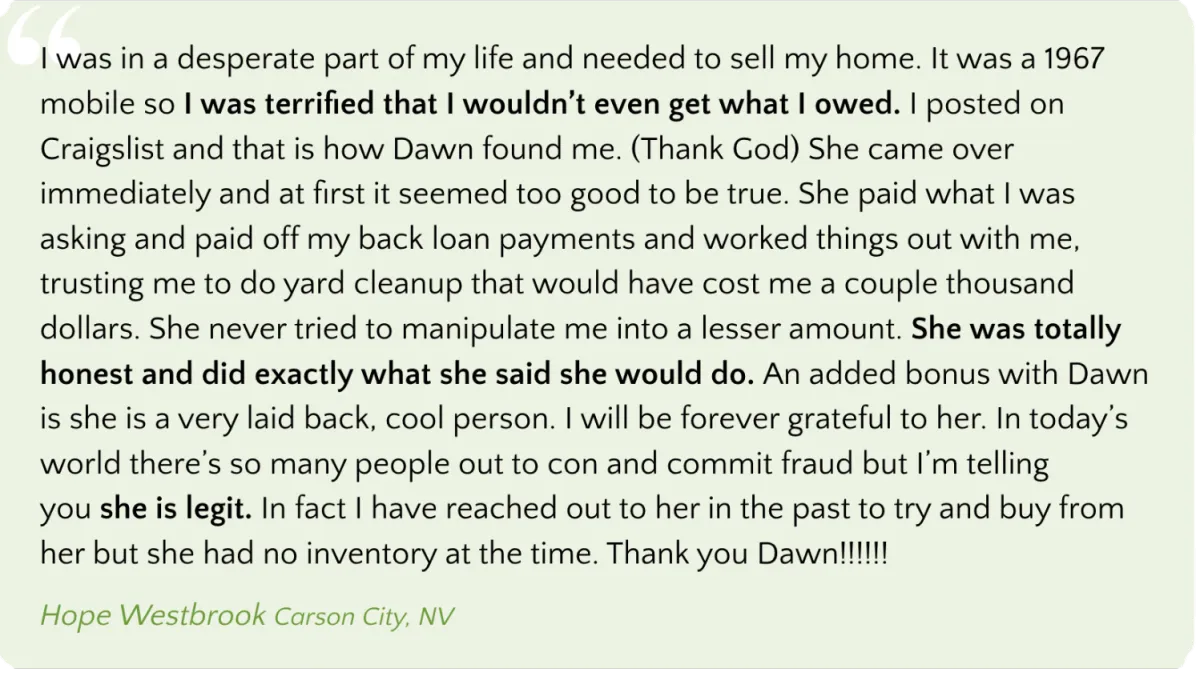

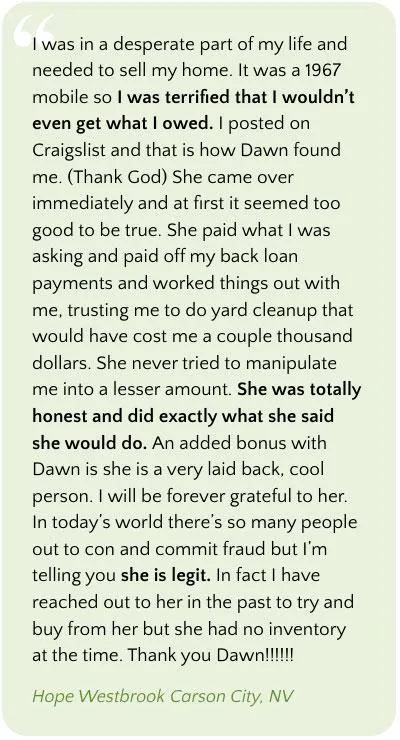

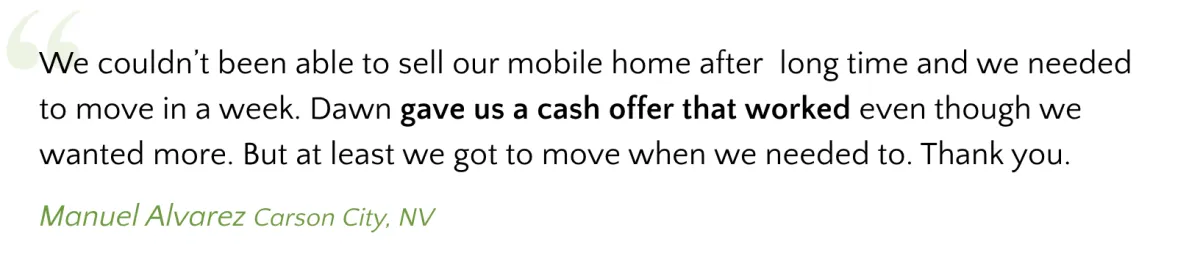

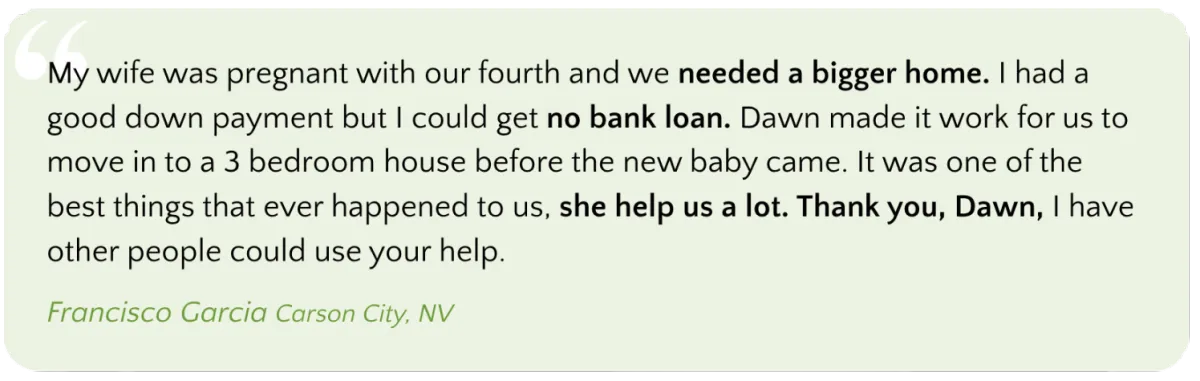

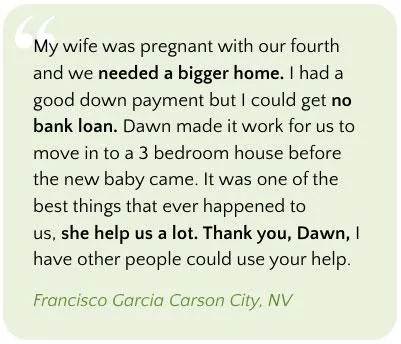

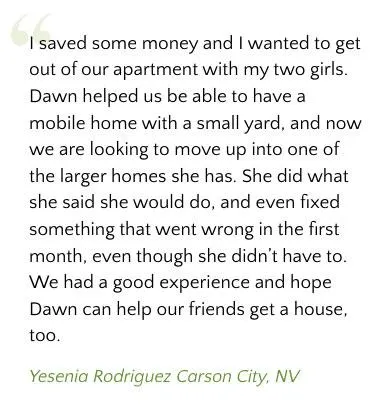

Featured Testimonials

Latest NQ Capital Articles